VLDB2024_TFB:Towards Comprehensive and Fair Benchmarking of Time Series Forecasting Methods_华为.pdf

免费下载

TFB: Towards Comprehensive and Fair Benchmarking of Time

Series Forecasting Methods

Xiangfei Qiu

East China Normal

University, China

Jilin Hu

East China Normal

University, China

Lekui Zhou

Huawei Cloud Algorithm

Innovation Lab, China

Xingjian Wu

East China Normal

University, China

Junyang Du

East China Normal

University, China

Buang Zhang

East China Normal

University, China

Chenjuan Guo

East China Normal

University, China

Aoying Zhou

East China Normal

University, China

Christian S. Jensen

Aalborg University,

Denmark

Zhenli Sheng

Huawei Cloud Algorithm

Innovation Lab, China

Bin Yang

East China Normal

University, China

ABSTRACT

Time series are generated in diverse domains such as economic,

trac, health, and energy, where forecasting of future values has

numerous important applications. Not surprisingly, many forecast-

ing methods are being proposed. To ensure progress, it is essential

to be able to study and compare such methods empirically in a com-

prehensive and reliable manner. To achieve this, we propose TFB,

an automated benchmark for Time Series Forecasting (TSF) meth-

ods. TFB advances the state-of-the-art by addressing shortcomings

related to datasets, comparison methods, and evaluation pipelines:

1) insucient coverage of data domains, 2) stereotype bias against

traditional methods, and 3) inconsistent and inexible pipelines. To

achieve better domain coverage, we include datasets from 10 dier-

ent domains : trac, electricity, energy, the environment, nature,

economic, stock markets, banking, health, and the web. We also

provide a time series characterization to ensure that the selected

datasets are comprehensive. To remove biases against some meth-

ods, we include a diverse range of methods, including statistical

learning, machine learning, and deep learning methods, and we

also support a variety of evaluation strategies and metrics to ensure

a more comprehensive evaluations of dierent methods. To support

the integration of dierent methods into the benchmark and enable

fair comparisons, TFB features a exible and scalable pipeline that

eliminates biases. Next, we employ TFB to perform a thorough eval-

uation of 21 Univariate Time Series Forecasting (UTSF) methods

on 8,068 univariate time series and 14 Multivariate Time Series

Forecasting (MTSF) methods on 25 datasets. The results oer a

deeper understanding of the forecasting methods, allowing us to

better select the ones that are most suitable for particular datasets

and settings. Overall, TFB and this evaluation provide researchers

with improved means of designing new TSF methods.

This work is licensed under the Creative Commons BY-NC-ND 4.0 International

License. Visit https://creativecommons.org/licenses/by-nc-nd/4.0/ to view a copy of

this license. For any use beyond those covered by this license, obtain permission by

emailing info@vldb.org. Copyright is held by the owner/author(s). Publication rights

licensed to the VLDB Endowment.

Proceedings of the VLDB Endowment, Vol. 17, No. 9 ISSN 2150-8097.

doi:10.14778/3665844.3665863

PVLDB Reference Format:

Xiangfei Qiu, Jilin Hu, Lekui Zhou, Xingjian Wu, Junyang Du, Buang

Zhang, Chenjuan Guo, Aoying Zhou, Christian S. Jensen, Zhenli Sheng and

Bin Yang. TFB: Towards Comprehensive and Fair Benchmarking of Time

Series Forecasting Methods. PVLDB, 17(9): 2363 - 2377, 2024.

doi:10.14778/3665844.3665863

PVLDB Artifact Availability:

The source code, data, and/or other artifacts have been made available at

https://github.com/decisionintelligence/TFB.

1 INTRODUCTION

As part of the ongoing digitalization, time series are generated

in a variety of domains, such as economic [

36

,

75

], trac [

30

,

33

–

35

,

49

,

51

,

52

,

62

,

79

,

85

,

93

,

95

], health [

44

,

61

,

83

,

88

], energy [

1

,

29

],

and AIOps [

7

,

8

,

41

,

72

,

87

,

103

]. Time Series Forecasting (TSF)

is essential in key applications in these domains [

28

,

67

,

94

,

97

].

Given historical observations, it is valuable if we can know the

future values ahead of time. Correspondingly, TSF has been rmly

established as an active research eld, witnessing the proposal of

numerous methods.

Time series organize data points chronologically and are either

univariate or multivariate depending on the number of variables

in each data point. Accordingly, TSF methods can be classied as

either Univariate Time Series Forecasting (UTSF) or Multivariate

Time Series Forecasting (MTSF) methods. Among early methods,

Autoregressive Integrated Moving Average (ARIMA) [

4

] and Vector

Autoregression (VAR) [

82

] are arguably the most popular univari-

ate and multivariate forecasting methods, respectively. Subsequent

methods that exploit machine learning, e.g., XGBoost [11, 99] and

Random Forest [

5

,

59

] oer better performance than the early meth-

ods. Most recently, methods based on deep learning have demon-

strated state-of-the-art (SOTA) forecasting performance on a variety

of datasets [

10

,

12

,

14

–

16

,

50

,

60

,

64

,

70

,

89

,

91

,

92

,

96

,

101

,

102

,

104

].

As more and more methods are being proposed for dierent

datasets and settings, there is an increasing need for fair and com-

prehensive empirical evaluations. To achieve this, we identify and

address three issues in existing evaluation frameworks, thereby

advancing our evaluation capabilities.

2363

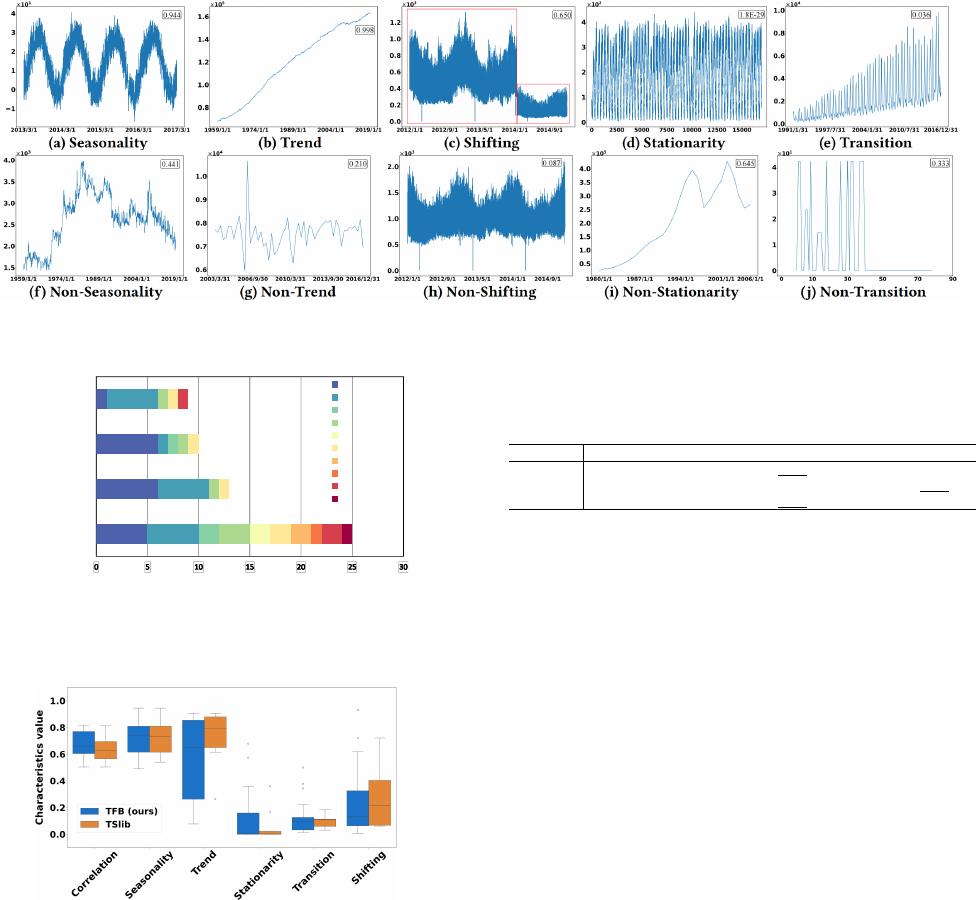

Figure 1: Visualization of data with dierent characteristics.

TFB (ours)

BasicTS+

BasicTS

TSlib &

LTSF-Linear

Datasets

Traffic

Electricity

Energy

Environment

Nature

Economic

Stock

Banking

Health

Web

Figure 2: Statistics of data domains covered by existing mul-

tivariate time series benchmarks.

Figure 3: Box plot of the variations in normalized values of

characteristics across the multivariate datasets in the TFB

and TSlib.

Issue 1. Insucient Coverage of Data Domains. Time series

from dierent domains may exhibit diverse characteristics. Fig-

ure 1a depicts a time series from the environment domain called

AQShunyi [

100

] that records temperature information at hourly

intervals, exhibiting a distinct seasonal pattern. This pattern is rea-

sonable in this scenario because temperatures in nature often cycle

around the year. Figure 1b shows a time series from FRED-MD [

58

]

belongs to economic domain that describes the monthly macroe-

conomic from 114 regional, national, and international sources

with a clear increasing tendency. This may be attributed to overall

Table 1: VAR, LR versus other methods, using MAE as the

evaluation metric and a forecasting horizon of 24 steps.

Datasets VAR LR

PatchTST NLinear FEDformer Crossformer

NASDAQ 0.462

0.616

0.567 0.522 0.547 0.745

Wind 0.620

0.583

0.652 0.640 0.697 0.590

ILI 1.012

4.856

0.835 0.919 1.020 1.096

economic stability with minimal uctuations, reecting sustained

growth in the macroeconomic indicators. Figure 1c depicts a se-

ries among Electricity [

84

] which comes from electricity domain

and has a signicant change in the data at a certain point in time,

which might indicate an abrupt event, etc. However, these sim-

ple patterns are only the tip of the iceberg, and time series from

dierent domains may exhibit much more complex patterns that

either combine the above characteristics or are entirely dierent.

Therefore, using only limited domains results in limited coverage

of time series characteristics, which cannot oer a full picture.

However, few empirical studies and benchmarks cover a wide

variety of data domains. Figure 2 summarizes the multivariate data

domains used in existing forecasting benchmarks which include

MTSF. We observe that TSlib [

89

], LTSF-Linear [

98

], BasicTS [

48

],

and BasicTS+ [

76

] only include around 10 datasets, covering less

than or equal to 5 domains. We observe that these datasets are

concentrated in mainly two domains, namely trac and electricity.

Since the multivariate time series datasets in TSlib are the most used,

we investigate the variations in the values of the characteristics

of datasets in TSlib and TFB—see Figure 3. We observe that the

TFB datasets exhibit more diverse distributions than those of TSlib

across the six characteristics. We argue that it is benecial to broaden

the coverage of domains, thereby enabling a more extensive assessment

of method performance.

Issue 2. Stereotype bias against traditional methods. It is dif-

cult for a single method to exhibit the best performance across

all datasets. Methods exhibit varying performance across dier-

ent datasets. To illustrate the issue, we conduct experiments on

three datasets (NASDAQ [

23

], Wind [

46

], and ILI [

90

]) from dier-

ent domains (stock markets, energy, health) on methods VAR [

82

],

PatchTST [

64

], LinearRegression (LR) [

32

,

40

], NLinear [

98

], FED-

former [

106

], and Crossformer [

101

]. Results are shown in Table 1.

2364

of 15

免费下载

【版权声明】本文为墨天轮用户原创内容,转载时必须标注文档的来源(墨天轮),文档链接,文档作者等基本信息,否则作者和墨天轮有权追究责任。如果您发现墨天轮中有涉嫌抄袭或者侵权的内容,欢迎发送邮件至:contact@modb.pro进行举报,并提供相关证据,一经查实,墨天轮将立刻删除相关内容。

下载排行榜

文档被以下合辑收录

评论